FOREIGN EXCHANGE MARKET DYNAMICS: WHAT ARE THE FACTORS THAT INFLUENCE THE EXCHANGE RATE? Part 1

January 2018

There are several major factors, in isolation or in tandem, which can impact the state of the foreign exchange market, and therefore the exchange rate.

These include:

- The current account balance

- Individual preferences of market participants

- International market conditions

- External shocks, and

- Inflation

THE CURRENT ACCOUNT: WE NEED TO EARN MORE THAN WE SPEND

The foreign exchange market, like all markets, functions generally on the basis of demand and supply, and so the exchange rate – the price of foreign exchange – will be determined accordingly.

The amount of foreign exchange available in the market is largely a function of how much we earn, and so if we try to spend more than we earn, by importing more than we export and receive from transfers, then that constitutes demanding more foreign exchange than what is available. That excess demand makes foreign exchange a scarce commodity, and prices rise and keep rising when commodities are scarce.

Fuelled by fiscal imbalances in the public sector, relatively low productivity in the private sector, and exacerbated by heavy dependence on imported oil and other inputs, Jamaica has for decades been in the position of earning less than we spend. This imbalance shows up in our balance of payments as a current account deficit, and for many years, those deficits were very high. Therefore, despite intervals of seasonal spikes in supply (often related to official borrowing), temporary periods of currency appreciation and despite monetary policy actions to support the local currency, this imbalance meant that the norm in the foreign exchange market, even at times of acclaimed “stability,” has been a sustained drift in one direction only.

Jamaica’s economic reform programme is geared to transition our import-dependent economy into one driven by the export of goods and services. As a result, we have already seen major and historic reductions in the current account deficit.

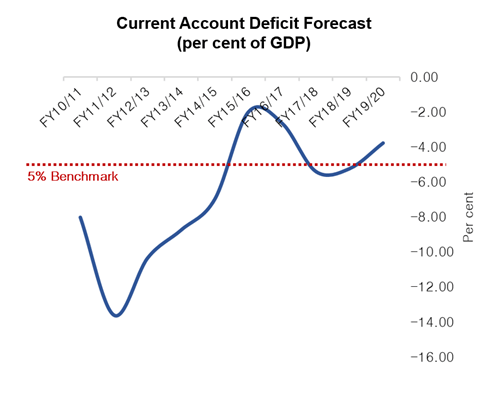

During one quarter in fiscal year 2015/16, we even posted a tangible surplus, while in more abstract terms, if we were to subtract from total imports the value of those imports financed by foreign direct investment, we would be seeing three straight calendar years of surplus at the end of 2017, a trend which is expected to continue. A current account deficit of around 4.5 to 5.0 per cent of GDP is considered sustainable by international standards, and Jamaica has recently been fluctuating between that region and as low as the region of 2.0 per cent of GDP, in stark contrast to a high of 18. 9 per cent of GDP in fiscal year 2008/09.

For the first time in many years, therefore, we are finally showing significant progress in closing and hopefully eventually reversing the gap between what we spend and what we earn. This is a major step in correcting the historical imbalance in our foreign exchange market, because a large balance of payments deficit is the major source of pressure on the exchange rate.

Removing that source of pressure, therefore, with increased exports and import substitution, automatically means a more buoyant foreign exchange market.

But, the logical question arises, if we are already correcting what was the major source of depreciation, then why do we still see some depreciation at times, even when our balance of payments position is in such good shape?

First of all, it is important to note that periodic gaps in supply and demand are a normal occurrence in a market. International trade is like any other business, and just like in any household or company, the payment of expenses does not always synchronize with the receipt of revenue. Delayed payment for a shipment of exported bauxite that coincides with paying for a large shipment of imported cars, for instance, could create a shortage of foreign exchange in a particular week, even if figures for the month overall show a surplus.

We should also remember that although the balance of payments position has been THE major factor, it is not the only factor which can impact the exchange rate.

INDIVIDUAL PREFERENCES OF MARKET PARTICIPANTS – IT IS A FREE MARKET.

When an exporter earns US$50 million dollars for a shipment of goods, it all counts as part of the country’s earnings, but does not automatically mean that all US$50 million, or indeed any at all, ends up in the foreign exchange market available for sale. It is a free market within a democracy, and so the exporter can save, invest, or spend the money as he or she chooses. Investors can also choose to invest in instruments denominated in foreign exchange or hold portions of their savings in foreign exchange.

What this means is that the full amount of foreign exchange that the economy earns does not always end up being available in the market, and so market demand can exceed supply even when overall economic numbers indicate that more than enough foreign exchange is available in the economy. People should always be able to choose what they do with their money, and so this factor will always exist and have to be accounted for. The solution to this particular possible imbalance is simply earning enough foreign exchange so that even after some people opt to hold foreign exchange in savings and investments, enough is still left over to supply demand in the market.

In addition, of course, this is where the importance of a central bank with adequate foreign exchange reserves comes in. When there are temporary imbalances because of issues like timing or portfolio choices, it is the central bank that periodically intervenes in the market to mitigate unusually large gaps in supply and demand.

Historically, because of an expectation that the local exchange rate is always going to depreciate and keep depreciating, there has been a tendency for foreign exchange earners to hold on to those earnings and convert only when they need to. The central bank has long maintained that when we get to the point where the foreign exchange market behaves like a normal healthy market instead of like an undernourished one, and the exchange rate regularly fluctuates up and down instead of recording a drift in one direction only, then market participants will feel less need to hoard foreign exchange.

Finally having that “normal healthy market” is exactly where we are now.

For example, during calendar year 2017, the exchange rate appreciated on 146 days and depreciated on 103. Over the same period in 2016, the exchange rate appreciated on only 66 days and depreciated on 183.

Also for calendar year 2017, the exchange rate appreciated by 2.7 per cent, compared to a depreciation of 6.2 per cent in 2016.

Recent Exchange Rate Movement

Once this status of exchange rate flexibility and stability is sustained, and gains are no longer guaranteed by holding foreign exchange, a greater percentage of earnings will be converted in a timely fashion. Individuals will feel more confident in saving and investing in Jamaican dollars and also more confident that foreign exchange will be available whenever they want to buy.

Bank of Jamaica