Summary of

Monetary Policy Discussion and Decision

March 2022

Bank of Jamaica’s Monetary Policy Committee (“MPC/the Committee”) sets monetary policy to meet the inflation target of 4.0 per cent – 6.0 per cent, as outlined by the Minister of Finance in April 2021.

At its meetings on 25 and 28 March 2022, the MPC noted that inflation continued to breach the upper limit of the Bank’s target range in February 2022 and would continue to breach the target range for a more extended period and at higher rates than previously anticipated. The Committee also noted that the invasion of Ukraine by Russia has increased the level of uncertainty in the environment, has significantly increased international commodity prices and has contributed to a further rise in domestic inflation and inflation expectations. Moreover, the MPC noted that the conflict posed a downside risk to domestic growth.

The MPC also noted that, in the wake of its monetary policy adjustments, while interest rates in the money market continued to increase and liquidity has tightened (as reflected in the decline in overnight placements or liquid balances by deposit-taking institutions at Bank of Jamaica), interest rates on new bank deposits and loans have only risen marginally. In the context of the Bank’s intervention in the foreign exchange market and the tightening of liquidity, the exchange rate has also reflected greater stability relative to the recent past. The Bank’s international reserves have also remained strong, which underpins the Bank’s capacity to support the foreign exchange market when necessary.

To continue limiting the second-round effects of the ongoing and protracted commodity price shock and guide inflation back to the target range over the next two years, the MPC unanimously agreed to increase the policy rate by 50 bps to 4.50 per cent. The Committee also decided to continue pursuing other measures to contain Jamaican dollar liquidity expansion and maintain relative stability in the foreign exchange market. These measures will cause liquidity conditions to remain tight and interest rates on deposits and loans to rise further, making savings in Jamaican dollars more attractive relative to foreign currency assets and borrowing in Jamaican dollars more expensive. This increase will also temper the demand for foreign currency, hence moderating the pace of depreciation in the exchange rate and reducing demand in the economy generally and, consequently, the ability of businesses to pass on price increases to consumers.

The MPC noted that it is prepared to take further appropriate actions at its next meeting depending on the incoming data.

The following considerations informed the Committee’s decisions:

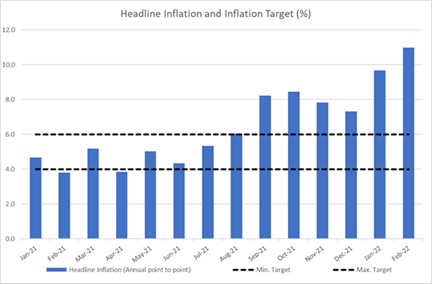

- The annual point-to-point inflation rate at February 2022 was 10.7 per cent, above the Bank’s forecast, the January 2022 outturn of 9.7 per cent and the Bank’s target range (see chart below). The acceleration in inflation, relative to January 2022, primarily reflected the effects of higher inflation for meats, transport services and agricultural commodities, consequent on elevated import prices of fertilizers, animal feed and fuel, etc. There were increases in all the major divisions of the consumer price index (CPI) during February, except for Education, Insurance and Financial Services and Information & Communication.

- In February 2022, Bank of Jamaica had projected inflation to average 6.0 to 7.0 per cent over the next two years, which was higher when compared to the average inflation rate of 5.5 per cent over the past two years. Inflation was projected to successively breach the upper limit of the Bank’s target range over the next 8 – 10 months, peaking in the range of 9.0 to 11.0 per cent. Conditional on the gradual tightening of monetary conditions, inflation was projected to return to the Bank’s target range of 4.0 to 6.0 per cent by end-2022.

- The risks to this inflation forecast are skewed to the upside (which means that actual inflation could track above the forecast). The major upside risk is higher-than-projected increases in international commodity and shipping prices and their impact on domestic prices. Average oil prices for the month to 28 March 2022 were approximately US$25 per barrel (or 30 per cent) above the Bank’s projection for the month. Similarly, average grains prices for the month to 25 March 2022 were 23.4 per cent above projections. The risk from international commodity prices largely emanates from the invasion of Ukraine by Russia and the imposition of economic and financial sanctions on Russia by Western industrialized nations, which has stimulated higher volatility in international energy, commodity and financial markets. The impact of shocks to international commodity prices is reflected in the annual change in the Jamaican producer price index for the manufacturing sector at January 2022 of 22.1 per cent, compared to average increases of 3.0 per cent for the past five years prior to the pandemic. Business expectations of inflation also remain elevated and have increased further. Finally, higher inflation among Jamaica’s main trading partners and the impact of adverse weather on agricultural food prices pose further upside risks to the inflation forecast.

- On the other hand, downside risks (which means that actual inflation could track below the forecast) include lower domestic demand in the context of the conflict. Significantly higher oil and grains prices could compress external demand for Jamaican goods and services (particularly tourism), putting downward pressure on domestic demand.

- An assessment of the risks to the domestic GDP growth forecast suggests that while GDP growth will fall in the projected range of 2.0 to 4.0 per cent for FY2022/23, it is now likely to be closer to the lower end of the forecast range. The principal downside risks to the forecast for GDP growth are the adverse impact of the Russia/Ukraine conflict on the services industries, particularly tourism and related services, and the worsening of already-impaired supply chains. In addition, new waves of the Covid-19 virus and the impact of higher inflation on real incomes could have an adverse impact on GDP growth.

- GDP growth in the United States (US) is likely to be lower than projected. This is mainly due to the continued shortage of key production inputs and higher inflation weighing on demand. Inflation in the US accelerated to 7.9 per cent at February 2022, above the target of 2.0 per cent, and is projected to remain elevated for some time.

- Against this background, the MPC noted the decision by the Federal Reserve Board (Fed) on 16 March 2022 to increase the benchmark federal funds rate by 25 bps. The Fed also signalled that the policy rate would increase faster in 2022 than originally projected. This signal supports the MPC’s decision to increase domestic interest rates further.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near term.

Chairman of the MPC

29 March 2022