Summary of

Monetary Policy Discussion and Decisions

November 2024

At its meetings on 19 and 20 November 2024, the Monetary Policy Committee (MPC) noted the following:

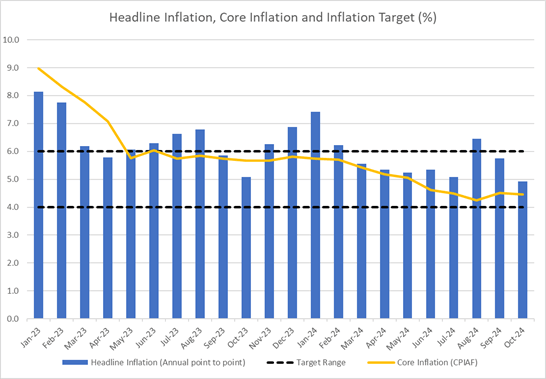

- Inflation is becoming more anchored in the Bank’s target range following the temporary impact of Hurricane Beryl on prices. Annual headline inflation at October 2024, as reported by the Statistical Institute of Jamaica (STATIN), was 4.9 per cent, lower than the 5.7 per cent at September 2024. This outturn was also lower than the most recent forecast and was within the Bank’s target range of 4.0 to 6.0 per cent. Core inflation (which excludes the prices of agricultural food products and fuel from the CPI) was 4.5 per cent at October 2024, representing the sixteenth consecutive month that core inflation was below 6.0 per cent.

- Inflation is projected to remain broadly within the Bank’s target range over the next two years. The key drivers of headline inflation, such as international grains prices and inflation in the economies of Jamaica’s main trading partners, continue to decline.In addition, the private sector’s expectations about the level of future inflation are gradually trending down. Despite an uptick in the exchange rate over recent months, the foreign exchange market remains relatively stable, supported by the Bank’s use of its buoyant foreign reserves to augment flows in the market.

- The risks to the inflation forecast are skewed to the upside. Uncertainty related to potential economic policy changes among Jamaica’s main trading partners could have adverse implications for investment and remittance inflows, as well as inflation expectations. Higher inflation could also result from further escalation in geopolitical tensions, which could negatively impact international supply chains. Worse-than-anticipated weather conditions in Jamaica could also put upward pressure on inflation. While anecdotal information suggests that private sector wage increases have stabilised at their pre-COVID rate, reports of labour market pressures in selected sectors have emerged. On the downside, lower inflation could result from weaker-than-projected demand.

- Against the background of these developments, the MPC at its meetings on 19 and 20 November 2024, assessed that the prevailing economic environment is conducive to a further easing of its monetary policy stance and unanimously agreed to: (i) reduce the policy rate by 25 basis points (bps) to 6.25 per cent per annum, effective Friday, 22 November 2024; and (ii) preserve relative stability in the foreign exchange market. The decision of the MPC to ease monetary policy further is based on an improvement in the inflation outlook.

The following considerations also informed the MPC’s decisions:

- The international prices of grains (including wheat, corn and soybeans) during the September 2024 quarter were lower, on average, by approximately 25.3 per cent, compared to the September 2023 quarter. Inflation in the United States (US) fell to 2.4 per cent at September 2024 from 3.7 per cent a year earlier, and from 8.2 per cent at September 2022. For Jamaica, lower grains prices and lower US inflation reduce the pace of increase in import costs. Lower US inflation also increases the likelihood of a further reduction in interest rates in the US. Energy and shipping prices also declined in the September 2024 quarter, but are projected to rise given geopolitical risks.

- In BOJ’s September 2024 survey of businesses’ inflation expectations, respondents lowered their expectations for inflation 12-months ahead to 7.6 per cent from 8.2 per cent, a continuation of a downward trend since the middle of 2022. As reflected in responses to survey questions, expectations about exchange rate depreciation have remained relatively stable. In this context, the dollarisation of deposits in commercial banks continues to be stable, generally in line with pre-COVID-19 levels.

- For fiscal year (FY) 2024/25, the Bank projects that real economic activity will be in the range of -1.0 to 0.5 per cent, while real GDP for FY2025/26 is projected to grow by 1.0 to 3.0 per cent. The projection for FY2024/25 largely reflects the anticipated adverse impact of Hurricane Beryl on the economy and is underpinned by contractions for Agriculture, Forestry & Fishing and Construction. The outlook for FY2025/26 reflects a partial rebound in economic activity following the declines in FY2024/25.

- The domestic banking system remains sound, with adequate capital and liquidity.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near-term.

- Given the potential implications for the foreign exchange market of the uncertainty noted above, the MPC reaffirmed its commitment to ensuring continued stability in the market. It also noted that, based on available information, future interest rate adjustments will, of necessity, be gradual and will continue to depend on the incoming data.

_______________________

Chairman of the MPC

21 November 2024