Summary of

Monetary Policy Discussion and Decisions

March 2026

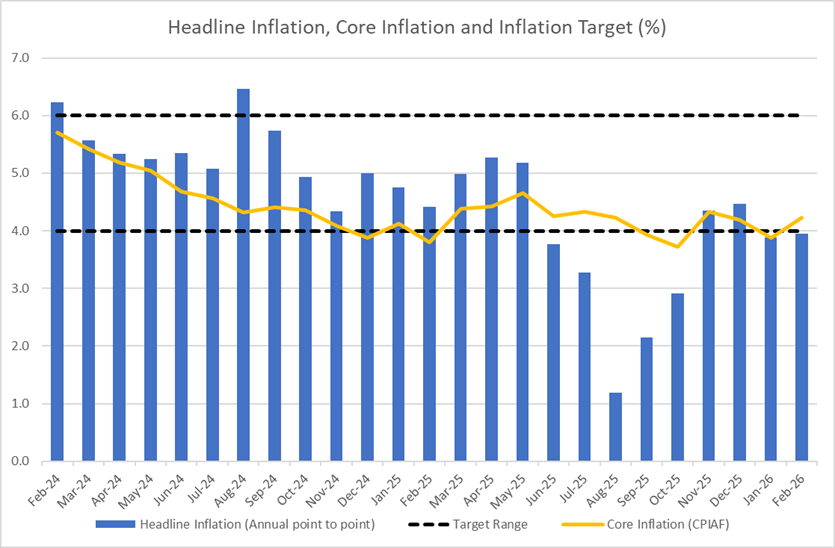

The Monetary Policy Committee (MPC) of Bank of Jamaica (BOJ), during its meetings on 27 and 30 March 2026, noted that while inflation remained below the lower limit of the Bank’s 4.0 to 6.0 per cent target range at February 2026, the inflation outlook is now subject to a high degree of uncertainty. The elevated level of uncertainty stems largely from the conflict in the Middle East, which has led to significant increases in key international commodity prices, particularly energy-related prices. The Committee noted that the shock to commodity prices poses a risk of higher domestic inflation and lower domestic growth. In the context of increased uncertainty, the MPC determined that the current monetary policy stance is the most appropriate to support inflation converging to the target range over time.

The MPC noted that the decision to maintain the policy rate is based on the following factors:

- Recent developments suggest that headline inflation will generally trend upward from 3.9 per cent at February 2026 and could exceed the inflation target during the year. Core inflation is also expected to trend above the Bank’s target range during 2026. This upward trajectory for inflation is driven by the conflict in the Middle East, which has led to sharp increases in international commodities prices (in particular, oil, liquefied natural gas (LNG) and fertiliser) and shipping costs; this is expected to influence higher energy and transport-related inflation in the domestic economy. Both the magnitude and the duration of the impact of these developments on inflation in Jamaica are, however, highly uncertain. In addition, inflation will be affected by the Government’s tax measures.

- The risks to the projected path for inflation over the next eight quarters are skewed to the upside (which means that inflation could be higher than the Bank’s projection). The major upside risk is an extended and broader conflict in the Middle East, resulting in further increases in international commodity prices and their resulting impact on domestic prices. In addition, higher-than-projected inflation expectations (what consumers and businesses expect inflation to be in the future) could contribute to inflationary pressures. Further, upward price pressures may arise from stronger-than-anticipated impact of higher domestic spending amid the post-hurricane recovery efforts. On the downside, the impact of these factors on prices could be tempered by reduced demand as a result of weaker consumer purchasing power.

Consequently, the Committee unanimously decided to: (i) maintain the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current account balances at BOJ) at 5.50 per cent per year; and (ii) continue special measures, including directly supplying the foreign exchange needs of selected players in the energy sector, to preserve stability in the foreign exchange market.

The following considerations also informed the MPC’s decisions:

- An assessment of the risks to the domestic growth forecast suggests that, while growth in gross domestic product (GDP) is likely to be within the projected range of 1.0 to 3.0 per cent for fiscal year (FY) 2026/27, there are downside risks to the forecast. The primary risk to the forecast for GDP growth is the adverse impact of the Middle East conflict on the services industries, particularly tourism and related services.

- The Federal Reserve (Fed) maintained its monetary policy target for interest rates within the target range of 3.50 to 3.75 per cent in March 2026. The Fed Chair noted that available indicators suggest that economic activity has been expanding at a solid pace and that the unemployment rate has somewhat stabilised. However, at the same time inflation remains elevated.

- The outturns for selected external indicators were mixed as oil and average grains prices increased, while prices declined for LNG. The daily West Texas Intermediate (WTI) crude oil prices for March 2026-to-date increased by 39.5 per cent relative to the previous month, a larger increase than the Bank’s previous projection. This is supported by increased concerns about supply amid the ongoing conflict in the Middle East. For March 2026-to-date, US LNG prices declined by 2.6 per cent relative to the previous month, a smaller decline compared to the previous projection. The fall in LNG prices is due to expectations for a build-up in LNG inventories arising from milder-than-forecast temperatures in February 2026 that left more natural gas in storage than expected during that period. Average grains prices (wheat, corn and soybean) increased in March 2026-to-date by 4.2 per cent relative to the previous month, compared with no change previously projected by the Bank. International fertiliser prices increased by 20.3 per cent for March 2026.

- Private-sector credit growth moderated in January 2026 to 6.9 per cent from 8.0 per cent in December 2025, reflecting a moderation in credit to individuals and businesses. Individual and business lending grew by 7.6 per cent and 6.2 per cent, respectively, in January 2026 from 9.2 per cent and 7.8 per cent in December 2025.

- The domestic banking system remains sound with adequate capital and liquidity.

- The domestic fiscal policy stance poses some risk to inflation over the near term.

- Amid the heightened uncertainty, Jamaica’s high levels of foreign reserves continue to provide a strong buffer, ensuring the availability of adequate levels of foreign exchange in the market.

- The Committee will continue to closely monitor the incoming data and assess their impact on inflation and inflation expectations. The MPC is prepared to take the necessary policy actions if the conflict in the Middle East becomes protracted and influences later price increases (i.e. second-round effects), that would further threaten the 4.0 to 6.0 per cent inflation target.

___________________

Richard Byles

Chairman of the MPC

31 March 2026