![]()

![]() Summary of

Summary of

Monetary Policy Discussion and Decisions

May 2026

During its meetings on 19 and 20 May 2026, the Monetary Policy Committee (MPC/“the Committee”) of Bank of Jamaica (BOJ) noted that the inflation outlook remains highly uncertain amid continued significant increases in key international commodity prices, particularly crude oil, arising from the ensuing conflict and tension in the Middle East. The Committee assessed that the global situation presented heightened risks to inflation in Jamaica, while also restraining domestic economic activity over the near term. Notwithstanding this shock, headline inflation is forecast to moderate as geopolitical tensions ease. The MPC consequently determined that maintaining the current monetary policy stance remains appropriate to limit later (second-round) price increases resulting from higher international commodity prices.

The MPC noted that the decision to maintain the policy rate is based on the following factors:

- Since the Bank’s assessment in March 2026, the Middle East conflict has deepened, with more extensive damage to critical oil infrastructure and supply chain disruptions. As a result, international fuel prices are projected to remain elevated over the near term. This is expected to place upward pressure on electricity costs in Jamaica. Domestic gas prices have already risen and may accelerate further, with implications for transport-related inflation. Beyond these direct effects, higher energy and transport costs are expected to contribute to second-round increases in the prices of goods and services across the economy.

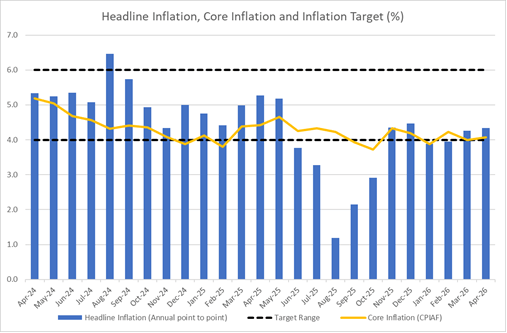

- Against this background, headline inflation is forecast to trend upward over the June 2026 and September 2026 quarters, from the 4.3 per cent at April 2026, and breach the 4.0 to 6.0 per cent per year inflation target range. The extent of the breach will depend on the severity and duration of the conflict, which are highly uncertain. Headline inflation is forecast to gradually moderate thereafter and return to the Bank’s target range as geopolitical tensions ease. This moderation will be driven by global oil supplies returning to normal levels. The projected moderation in inflation is also expected to be partly offset by domestic demand pressures, stemming primarily from fiscal spending to support rebuilding efforts following Hurricane Melissa.

- The risks to the inflation forecast are assessed to be skewed to the upside, which means that inflation could be higher than projected. The main upside risk is a more extended and broader conflict in the Middle East, resulting in further increases in international commodity prices and their subsequent impact on domestic prices. In addition, adverse weather conditions, including the effects of El Niño, could place upward pressure on agricultural prices. Higher-than-projected inflation expectations could also contribute to inflationary impulses. Further, higher inflation may arise from a stronger-than-anticipated impact of higher domestic spending amid the post-hurricane recovery activities. On the downside, the impact of these factors on prices could be tempered by reduced demand because of weaker consumer purchasing power.

The Committee, therefore, unanimously decided to: (i) maintain the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current account balances at BOJ) at 5.50 per cent per year; and (ii) continue special measures to preserve stability in the foreign exchange market, including directly supplying the foreign exchange needs of selected entities in the energy sector and the pre-announced sale of foreign exchange into the market.

The following considerations also informed the MPC’s decisions:

- The Statistical Institute of Jamaica reported that annual headline inflation at April 2026 was 4.3 per cent, in line with the outturn recorded in the previous month but above the Bank’s projection. The stable inflation when compared with March 2026, was due mainly to higher prices for some agricultural produce offset by lower electricity rates. However, core inflation was 4.1 per cent at April 2026, which was above the outturn of 4.0 per cent at March 2026.

- Growth in real gross domestic product (GDP) for fiscal year (FY) 2026/27 is projected within the range of 1.0 to 3.0 per cent. The risks to the GDP outlook are skewed to the downside, reflecting the potential adverse effects of the conflict in the Middle East on the services industries, particularly tourism and related activities. In addition, higher input costs associated with imported inflation are likely to weigh on domestic economic activity.

- The Federal Reserve (Fed) maintained its monetary policy target for interest rates within the target range of 3.50 to 3.75 per cent in April 2026. The Fed Chair noted that job gains remained low and that the unemployment rate has somewhat stabilised with economic activity expanding at a solid pace. However, inflation was elevated, in part reflecting the recent increase in global energy prices. Further, the Fed Chair noted that the economic outlook was uncertain due to developments in the Middle East.

- Imported inflation increased in the March 2026 quarter, relative to the December 2025 quarter. Inflation in the United States increased to 3.3 per cent at March 2026 from 2.4 per cent a year earlier. West Texas Intermediate (WTI) crude oil prices for the quarter rose by 21.5 per cent relative to the previous quarter and are projected to remain elevated over the next two years. The increase in oil prices is supported by supply concerns amid ongoing geopolitical tensions in the Middle East. Further, average grains price (including wheat, corn and soybeans) for the quarter increased by 5.2 per cent, compared with the December 2025 quarter, while shipping prices grew by 13.0 per cent. Over the near term, average oil and grains prices are forecast to increase by 13.6 per cent and 3.4 per cent per year, respectively.

- In the April 2026 survey of businesses’ inflation expectations, respondents increased their expectations for inflation 12 months ahead to 7.1 per cent relative to 6.5 per cent in the prior survey. In addition, respondents increased their expectations about exchange rate depreciation. The dollarisation ratio for deposits in commercial banks, a measure of the public’s view about exchange rate risk, however, continues to be relatively stable.

- Private sector credit growth continued to moderate in the March 2026 quarter to 6.5 per cent from growth of 7.8 per cent in the December 2025 quarter. The moderation is driven by a slowdown in credit to both businesses and individuals. For the March 2026 quarter, lending to individuals and businesses grew by 7.5 per cent and 5.1 per cent, respectively, relative to growth of 8.3 per cent and 7.5 per cent in the December 2025 quarter.

- The domestic banking system remains sound with adequate capital and liquidity.

- The domestic fiscal policy stance poses some risk to inflation over the near term.

- The negative impact of the conflict on the external accounts is expected to be significant. However, the Committee noted that the Bank’s strong foreign reserves provide an important buffer against external shocks. Reserve levels are expected to remain adequate over the medium term and will support the orderly functioning of the foreign exchange market, helping to limit volatility and thereby containing imported inflation.

- The Committee will continue to closely monitor the incoming data and assess the implications for inflation and inflation expectations. The MPC is prepared to adjust its monetary policy stance if the conflict in the Middle East is protracted, resulting in sustained price increases.

___________________

Richard Byles

Chairman of the MPC

20 May 2026