Summary of

Monetary Policy Discussion and Decisions

December 2025

During its meetings on 16 and 17 December 2025, Bank of Jamaica’s (BOJ’s) Monetary Policy Committee (MPC) expressed concern that the impact of Hurricane Melissa on the economy was more pronounced than initially anticipated, creating a greater risk that the inflation impact could be larger.

More recent estimates indicate that damage to roads, buildings, the electricity grid and other infrastructure is in excess of 40 per cent of gross domestic product (GDP), above the previous estimate of 30 per cent. The Agriculture sector experienced damage amounting to approximately 50 per cent of the sector’s 2024 GDP. The larger damage means that initial impact on agriculture and electricity prices, as well as the later effect on the prices of other goods and services (the second-round impact) of this initial jump, is likely to be stronger and more persistent than initially anticipated. As a result, the upside risk of the disaster on the inflation outlook is greater, meaning that inflation could be higher than forecast.

Against this background, the Committee decided unanimously to (i) continue holding the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current account balances at BOJ) at 5.75 per cent per annum, and (ii) remain proactive in preserving relative stability in the foreign exchange market.

The decision to continue holding the policy rate at this time is based on the following factors:

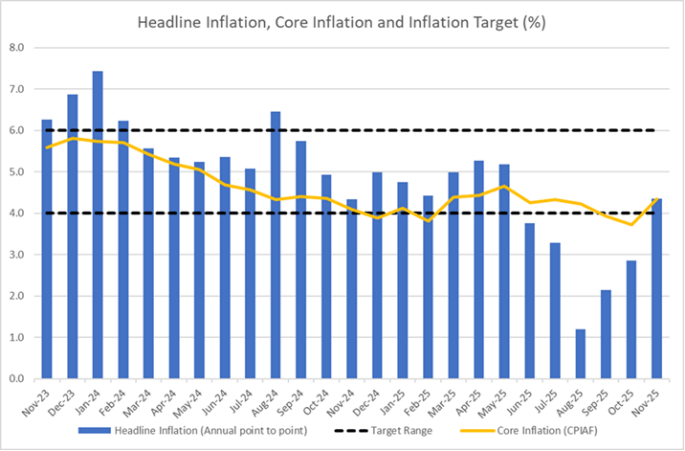

- Annual headline inflation will rise sharply over the next few months from 4.4 per cent at November 2025 and remain elevated for the near-term. In this context, inflation will exceed the Bank’s inflation target of 4.0 to 6.0 per cent by early 2026. This rise primarily reflects the hurricane’s impact on the major food-producing parishes and disruptions to supply chains (particularly in energy and agriculture), which monetary policy cannot affect.

- Core inflation (which excludes the prices of agricultural food products and fuel from the consumer price index (CPI)) will also rise over the next twelve months, reflecting another wave of price increases for other goods and services (e.g. those related to home repairs, meals from restaurants and personal care items) through second-round effects. The Bank is therefore positioning monetary policy to minimise such effects and to constrain increases in inflation expectations (i.e. what businesses and consumers anticipate will happen to retail prices). The higher core inflation will be supported by the anticipated surge in overall spending in the context of the rebuilding efforts, financed largely by external financing to the private and public sectors.

- In the aftermath of the hurricane, Parliament has suspended the fiscal rule for an initial period of one year. This will support the public sector’s ability to increase spending for the recovery and relief effort. For the central government in particular, larger fiscal deficits are projected over the next three fiscal years, compared with their previous projection.

- The risks to the inflation outlook are skewed to the upside with a greater likelihood of inflation being above projections. Higher inflation could result from higher-than-expected demand amidst the reconstruction efforts and from increased inflation expectations. A more protracted recovery in the agriculture sector and more prolonged disruptions to supply chains could worsen food price increases. There could also be long-term damage in specific industries, which could slow the improvement in the production and availability of supplies. On the downside, inflation could be lower due to a slower-than-anticipated recovery in domestic demand associated with income loss.

The following considerations also informed the MPC’s decisions:

- The Statistical Institute of Jamaica reported that annual headline inflation at November 2025 was 4.4 per cent above the Bank’s projections and above the 2.9 per cent at October 2025. The higher inflation compared with October 2025, was due mainly to higher food prices, reflecting early signs of the impact of the hurricane on the Agriculture sector. Core inflation was 4.3 per cent at November 2025, which was above the outturn of 3.7 per cent at October 2025.

- Economic activity will contract significantly in the immediate aftermath of the hurricane. In this context, the Bank anticipates a decline in real GDP in the range of -4.0 to -6.0 per cent for fiscal year (FY) 2025/26, largely due to the extensive damage to infrastructure and disruption to productive activity. BOJ projects that the financial inflows from multilateral and private sources will support spending in the economy over the next three years, to the extent that the capacity exists to execute planned projects. For FY2026/27, real GDP growth is projected in the range of -1.0 to 1.0 per cent, reflecting the commencement of recovery efforts, which will escalate in ensuing years.

- Although the current account of Jamaica’s balance of payments is projected to deteriorate over the near-term, the international reserves will remain robust.

- The United States (US) Federal Reserve (Fed) reduced its monetary policy target for interest rates by 25 basis points to a target range of 3.50 to 3.75 per cent in December 2025. The Fed Chair noted that while economic activity has been expanding at a moderate pace, the unemployment rate has increased. At the same time, inflation has increased and remains somewhat elevated. The Fed Chair noted that with the target range now within the range of estimates for its neutral value, it is well positioned to base future monetary policy decisions on incoming data.

- The outturns for selected external indicators were mixed as oil prices declined while grains and liquefied natural gas (LNG) prices increased. The average of daily West Texas Intermediate (WTI) crude oil prices for October and November 2025 declined by 3.3 per cent, a larger decline than the Bank’s forecast at the last projections. Prices marginally declined in December 2025 to date, supported by market’s expectation for an increase in global production in 2025 and 2026. For LNG, average prices for October and November 2025 increased by 22.4 per cent, relative to the projection for a smaller increase over the period. This is supported by increased demand amid winter weather conditions. Average grains prices (wheat, corn and soybean) increased for October and November 2025 by 3.8 per cent, compared with the Bank’s projection for a decline for the period. International fertiliser prices, declined by 2.8 per cent in October 2025.

- The domestic banking system remains sound with adequate capital and liquidity.

- The domestic fiscal policy stance poses some risk to inflation over the near-term.

- The MPC reaffirms its view that preserving a stable macroeconomic environment is essential to the country’s recovery and reconstruction efforts. BOJ, therefore, remains committed to ensuring that the inflationary effects of the hurricane are managed to limit hardships on vulnerable groups and to facilitate the conditions necessary for long-term economic recovery.

- The Committee will continue to closely monitor the incoming data and maintain heightened surveillance of the second-round impact of higher food prices on core inflation. The MPC is prepared to adjust the stance of monetary policy and to take the necessary policy action, if the above-noted risks threaten the projected return of inflation to the target range in the shortest possible time.

___________________

Richard Byles

Chairman of the MPC

18 December 2025