Summary of

Monetary Policy Discussion and Decisions

February 2026

Bank of Jamaica’s (BOJ’s) Monetary Policy Committee (MPC), during its meetings on 19 and 20 February 2026, assessed that the direct impact of Hurricane Melissa on inflation was less severe than initially anticipated. A faster-than-expected improvement in agricultural supplies, along with recent mild exchange rate appreciation, supported lower inflation. Inflation is now projected to generally trend within target over the next eight quarters, with a few exceptions. In this regard, the MPC noted the following:

The inflation forecast takes into account an improved outlook for key domestic macroeconomic indicators. After possible temporary breaches of the upper limit of the inflation target over the June and September 2026 quarters, inflation is now projected to return to the 4.0 to 6.0 per cent target range by the end of the December 2026 quarter. This earlier-than-previously-anticipated return to target reflects a moderation of the Bank’s forecast for later (or second-round) price increases. In addition, private sector expectations of future inflation (inflation expectations), a key driver of headline inflation, are forecast to fall to normal levels over the near term. The current account of Jamaica’s balance of payments is, however, projected to record higher deficits over the near term as the economy rebuilds from the Hurricane Melissa fallout, but the international reserves remain healthy and are projected to improve further. The forecast also considers the direct impact of the recently announced tax package.

In the context of the improved inflation outturn and outlook, the Committee decided unanimously to: (i) reduce the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current account balances at BOJ) by 25 basis points to 5.50 per cent per annum, effective 24 February 2026; and (ii) remain proactive in preserving relative stability in the foreign exchange market.

The decision to reduce the policy rate followed detailed consideration of a number of factors, including:

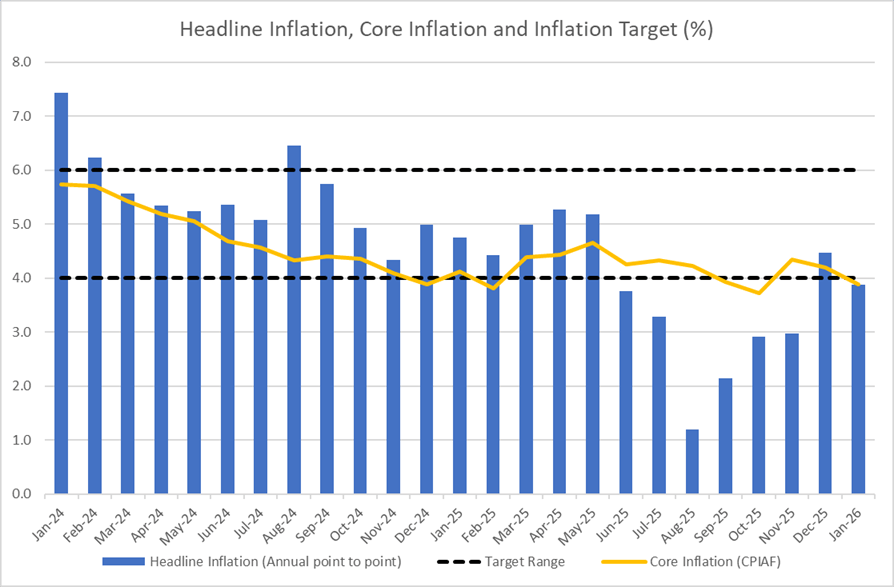

- The Statistical Institute of Jamaica reported that annual headline inflation at January 2026 was 3.9 per cent, lower than the Bank’s projection and the 4.5 per cent at December 2025. The lower inflation compared with December 2025 was due mainly to a decline in food prices, reflecting the impact of the improvement in agricultural supplies following Hurricane Melissa and an appreciation in the exchange rate. Core inflation (which excludes the prices of agricultural food products and fuel from the consumer price index (CPI)) was 3.9 per cent at January 2026, lower than the outturn of 4.2 per cent at December 2025.

- The risks to the inflation forecast are balanced. On the downside, inflation could be lower due to a slower-than-anticipated recovery in domestic demand. On the upside, higher inflation could result from more adverse weather as well as higher-than-projected inflation expectations. In addition, upward price pressures may arise from increased overall domestic spending amid the post-hurricane recovery efforts. In particular, the government’s temporary suspension of the fiscal rule will allow for fiscal deficits over the next three years. These deficits, in supporting higher spending in the economy, could place pressure on the country’s productive capacity and contribute to higher second-round price pressures.

The following considerations also informed the MPC’s decisions:

- For fiscal year (FY) 2025/26, the Bank anticipates a decline in real gross domestic product (GDP) in the range of -1.0 to -3.0 per cent, a smaller contraction than the previous estimate. As the economy recovers, real GDP growth for FY 2026/27 is projected in the range of 1.0 to 3.0 per cent. The risks to the outlook for GDP are skewed to the downside, meaning that GDP could be lower than projected.

- The United States (US) Federal Reserve (Fed) maintained its monetary policy target for interest rates within the target range of 3.50 to 3.75 per cent in January 2026. The Fed Chair noted that economic activity has been expanding at a solid pace and that the unemployment rate has shown signs of stabilisation. At the same time, inflation has stabilised but remains somewhat elevated.

- The outturns for selected external indicators were mixed as oil prices increased while average grains and liquefied natural gas (LNG) prices declined. The daily West Texas Intermediate (WTI) crude oil prices for January 2026 increased by 3.8 per cent relative to the previous month, a larger increase than the Bank’s previous projection. Crude oil prices also increased so far in February 2026, supported by increased concerns about supply amid ongoing geopolitical tensions between the US and Iran and a decline in US crude inventories. For January 2026, LNG prices declined by 4.5 per cent relative to the previous month, and compared with the increase previously projected by the Bank. This is supported by warmer weather conditions in early January 2026, which reduced the demand for heating gas. Following extreme weather events in mid-January 2026, prices normalised towards the end of the month. Average grains prices (wheat, corn and soybean) declined in January 2026 by 2.0 per cent relative to the previous month, and compared with the marginal increase previously projected by the Bank. International fertiliser prices increased by 11.8 per cent in January 2026.

- Since mid-2025, private sector credit growth has remained relatively stable with a recent uptick in December 2025. This stability is driven predominantly by credit to individuals, with a moderation in business lending. Annual growth in business lending averaged 8.7 per cent in 2025, compared with 10.9 per cent in 2024. Household credit growth has adjusted more gradually and has provided the main support to aggregate loan growth since mid-2025.

- The domestic banking system remains sound with adequate capital and liquidity.

- The domestic fiscal policy stance poses near-term risks to inflation.

- The Committee will continue to closely monitor the incoming data. The MPC is prepared to adjust the stance of monetary policy and to take the necessary policy action if the balance of risks shifts and threatens the projected return of inflation to the target range in the shortest possible time.

___________________

Richard Byles

Chairman of the MPC

23 February 2026