Summary of

Monetary Policy Discussion and Decisions

September 2025

The Monetary Policy Committee (MPC) of Bank of Jamaica (BOJ), during its meetings on 25 and 26 September 2025, deliberated on the Bank’s monetary policy stance in the context of continued low domestic inflation, global uncertainties and evolving interest rate trajectories in major developed countries. Following these deliberations, the MPC determined that the current policy stance continues to be appropriate to support inflation converging to the target range.

The MPC noted that the decision to maintain the policy rate is based on the following factors:

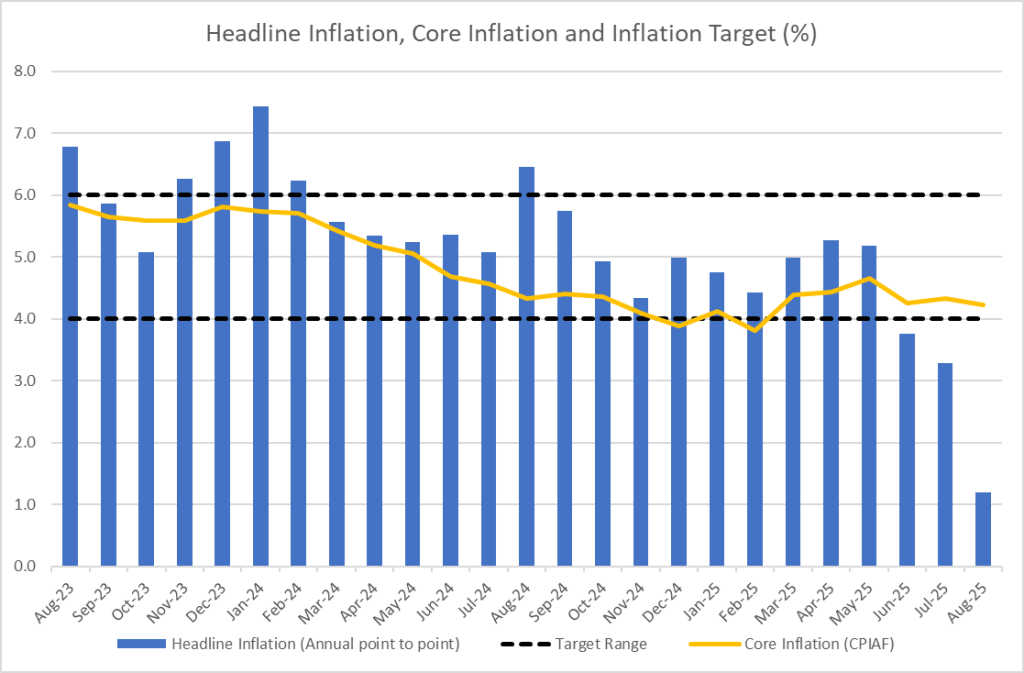

- While headline inflation of 1.2 per cent at August 2025 is below the Bank’s target range of 4.0 to 6.0 per cent, core inflation continues to track within the target range. Moreover, the causes of the low headline inflation rate at August 2025 are temporary.

- The low headline inflation rate at August 2025 is unrelated to demand conditions.

- The risks to the inflation outlook are skewed to the upside.

The following data informed the MPC’s decisions:

- The temporary factors that caused low headline inflation in August 2025 were primarily related to improvements in supply conditions. In particular, agricultural prices during the month were lower than a year earlier, when prices rose due to the negative impact of Hurricane Beryl on domestic crop production. Supplies improved subsequent to the adverse weather, leading to prices reverting to more normal levels. In addition, the dissipation of the impact of a previous adjustment in public transport fares, as well as a reduction in the General Consumption Tax (GCT) on electricity consumption announced by the Government in March 2025, contributed to lower-than-targeted inflation. Notwithstanding these temporary shocks, core inflation (which excludes the prices of agricultural food products and fuel from the Consumer Price Index (CPI)) was 4.2 per cent at August 2025, remaining within the target range since March 2025.

- The reduction in inflation at August 2025 occurred despite improvements in domestic demand. The economy grew in the March 2025 quarter and is estimated to have expanded in the June and September 2025 quarters. Growth for the September 2025 quarter is estimated in the range of 3.0 to 4.0 per cent. This continued expansion is consistent with a tight labour market and anecdotal information on elevated wage growth. Growth in the economy is expected to be maintained over the next two years.

- Recent developments suggest that headline inflation will continue to track below the lower limit of the Bank’s target range for the remainder of 2025 but should return to the target range by the March 2026 quarter. This upward trajectory is supported by the anticipated dissipation of the temporary shocks. Core inflation is projected to remain within the target range over the next two years consistent with stable inflation expectations and a growing economy.

- The risks to the projected path for inflation over the next eight quarters are skewed to the upside (which means that inflation could be above projections). Higher inflation could stem from a sharper-than-anticipated increase in tariffs faced by the United States’ (US’) trading partners as well as related second-round effects. This could result in higher imported inflation and inflation expectations. In addition, inflation could be higher than projected if there is further escalation in geopolitical tensions, which could negatively impact international supply chains. Lower inflation could, however, result from lower-than-projected international commodity prices as well as weaker demand conditions.

- Economic indicators continue to point to a stable macroeconomic environment. Further, with stable domestic interest rates, the decline in interest rates abroad has improved the differential between domestic and external rates, which should better support stability in the foreign exchange market. In addition, the current account of Jamaica’s balance of payments is projected to remain in surplus over the near term, and the international reserves are healthy and are projected to improve further.

- Against the background of these developments, the MPC, unanimously agreed to (i) hold the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current account balances at BOJ) at 5.75 per cent per annum, and (ii) continue taking measures to preserve relative stability in the foreign exchange market.

The following considerations also informed the MPC’s decisions:

- The outlook for real economic activity for fiscal year (FY) 2025/26 and FY2026/27 is likely to be in line with the last forecast. Preliminary indicators suggest that the economy should expand in the September 2025 quarter, resulting from expansions in electricity & water supply, agriculture and tourism and its allied services. Thereafter, economic activity is anticipated to strengthen throughout FY2025/26. In this context, real gross domestic product (GDP) is projected to recover in FY2025/26 in the range of 1.0 to 3.0 per cent, largely due to growth in the Agriculture, Mining, and Tourism sectors.

- In August 2025, headline inflation in the US increased to 2.9 per cent from 2.7 per cent in July 2025. Inflation in the US is projected to remain above the US Federal Reserve’s (Fed) target of 2.0 per cent for the remainder of 2025. For the June 2025 quarter, US GDP expanded by 3.3 per cent, reflecting increases in net exports and consumer spending. The growth in net exports was supported by a decline in imports due to the utilisation of goods stockpiled in anticipation of higher tariffs.

- The Fed reduced its monetary policy target for interest rates by 25 basis points to a target range of 4.0 to 4.25 per cent in September 2025. The Federal Reserve Chair noted that downside risks to employment have increased, while recent economic indicators suggest a moderation in the growth of economic activity during the first half of the year. At the same time, inflation has increased and remains somewhat elevated. The Fed noted that future monetary policy decisions will continue to be based on the incoming data.

- The outturns for selected external indicators including oil, grains and liquefied natural gas (LNG) prices declined. The average of daily West Texas Intermediate (WTI) crude oil prices for July and August 2025 declined by 2.7 per cent, a larger decline than the Bank’s forecast. Prices declined further in September 2025 to date, reflecting OPEC+’ decision to increase its crude oil production in October 2025 along with signs of weakening demand amid a moderation in US employment. For LNG, average prices for July and August 2025 declined by 11.2 per cent, relative to the projection for a smaller decline over the period. This is supported by a build up in US inventories. Average grains prices (wheat, corn and soybean) declined for July and August 2025 by 1.9 per cent, compared with the Bank’s projection for a smaller decline for the period. International fertiliser prices, on average, increased by 6.3 per cent over July and August 2025.

- BOJ’s July 2025 survey of businesses’ inflation expectations indicated that respondents expected inflation 12 months ahead to be 7.0 per cent, generally stable relative to 7.1 per cent in the previous survey.

- The domestic banking system remains sound with adequate capital and liquidity.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near term.

- The MPC reaffirms its commitment to maintaining low and stable inflation. To this end, the Committee will continue to monitor the incoming data and adjust its policy accordingly. This includes maintaining heightened surveillance of the trajectory of core inflation relative to the lower bound of the inflation target range. Moreover, the MPC remains committed to its work programme to further strengthen the policy transmission process.

___________________

Richard Byles

Chairman of the MPC

29 September 2025