Summary of

Monetary Policy Discussion and Decisions

June 2024

At its meetings on 26 and 27 June 2024, the Monetary Policy Committee (MPC) noted the following:

- Over the past three years, Bank of Jamaica (BOJ) has tightened monetary policy by utilising a three-pronged approach. Specifically, the Bank has: (i) increased the policy rate (the rate offered to deposit-taking institutions (DTIs) on their current accounts with the Central Bank)by 650 basis points (bps) to 7.0 per cent, resulting in small increases in DTIs’ loan rates and moderate increases in their deposit rates; (ii) tightened Jamaica dollar liquidity in the money market using its open market operations, which led to increases in private money market interest rates; and (iii) utilised its foreign reserves to maintain relative stability in the foreign exchange market.

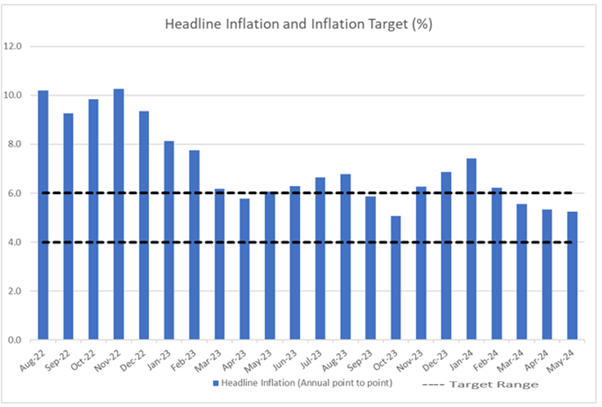

- This tight monetary policy stance was appropriate given that inflation had significantly increased from a low of 3.8 per cent at April 2021 to a high of 11.8 per cent at April 2022 and, thereafter, remained outside the target range of 4.0 to 6.0 per cent for several months. The Bank’s policy actions were designed to reduce inflation by constraining domestic aggregate demand and minimising the impact of imported inflation as a result of stability in the foreign exchange market.

- Incoming data now suggest that there has been significant success in the fight against high and unpredictable inflation in Jamaica. The Statistical Institute of Jamaica (STATIN), on 17 June 2024, reported that annual headline inflation at May 2024 was 5.2 per cent. This outturn represented the third consecutive month in which inflation fell within the Bank’s target range and the fourth consecutive month of decline in headline inflation. The outturn was also significantly lower than the Bank’s most recent forecast. Further, core inflation, which excludes all food types as well as fuel prices (including transport prices), from the Consumer Price Index (CPI)) was 5.6 per cent at May 2024, marginally lower than the previous month. Another measure of core inflation that excludes the prices of agricultural food products and fuel prices was 5.1 per cent at May 2024, also reflecting a downward trend closer to the mid-point of the Bank’s target range.

- The reduction in inflation has been largely due to some containment in domestic demand, a stable exchange rate and a decline in imported inflation. Additionally, inflation expectations have stabilised, and anecdotal information suggests that wage pressures have moderated. The MPC also noted the surplus on the current account of the balance of payments for the December 2023 quarter, as well as the positive outlook for the balance of payments over the next year. This surplus underpins the relatively strong flows in the foreign exchange market and the relative stability in the exchange rate.

- In this context, projected inflation will likely be revised downward and generally remain within the target range over the next two years, except for a few months in 2025. The projected breaches of the upper limit of the inflation target range in 2025 largely reflect an acceleration in agricultural price inflation, following sharp declines in March 2024.

- The risks to the inflation outlook are balanced (which means that inflation is likely to be in line with projections). These risks include rising international shipping costs and the possibility of worse-than-anticipated weather conditions due to the emerging La Niña weather phenomenon.

- Against the background of the improved inflation outlook, the MPC at its meetings on 26 and 27 June 2024, unanimously agreed to start a gradual easing of its monetary policy stance. The first step involves gradually reducing BOJ ’s absorption of liquidity from DTIs through open market operations, thereby facilitating: (a) the channelling of additional credit to the productive sector; and (b) gradual rate reductions in the money market. However, the MPC decided to maintain the policy rate at 7.0 per cent per annum, at this time, and to continue its proactive stance of preserving relative stability in the foreign exchange market.

The following considerations also informed the MPC’s decisions:

- The Jamaican economy continues to grow. Real gross domestic product (GDP) for the March 2024 quarter is estimated to have grown within the range of 1.5 to 2.5 per cent, and there are signs that the economy continued to expand in the June 2024 quarter.

- The risks to the domestic GDP forecast over the next eight quarters are assessed to be balanced, which means that actual GDP growth could be in line with the forecast. On the downside, escalations in geopolitical tensions could adversely affect global growth and, hence, external demand. Better-than-expected growth in the global economy could improve external demand.

- Inflation in the United States (US) was 3.3 per cent at May 2024, a deceleration relative to the April 2024 outturn of 3.4 per cent. Inflation in the US is projected to moderate as the economy slows but remain above the US Federal Reserve’s (Fed) target of 2.0 per cent for the remainder of 2024.

- The risks to the outlook for the US economy are skewed to the downside. Lower growth could emanate from a stronger-than-projected impact of contractionary monetary policy and the tightening of credit conditions on GDP growth. Additional downside risks include adverse weather conditions due to climate change, which could increase the risk of trade disruptions, escalating geopolitical tensions and the impact of higher taxes from the US administration. However, higher-than-projected increases in consumption spending could provide some partial offsetting impulses.

- As anticipated, the Fed maintained its monetary policy target for interest rates at 5.25 to 5.50 per cent in June 2024. The Fed also suggested that future monetary policy decisions will continue to be data-dependent.

- The outturns for selected external indicators were mixed. While average grains prices (wheat, corn, and soybean) declined by 1.2 per cent in April, prices increased by 4.4 per cent in May 2024. The average of liquefied natural gas (LNG) prices increased by 18.9 per cent for April and May 2024. The increase in LNG prices was supported by lower production in the US and greater external demand. However, the average daily West Texas Intermediate (WTI) crude oil prices for April and May 2024 declined by 1.1 per cent due to increased production in the US. International fertiliser prices, on average, declined over April and May 2024 because of falling demand.

- The MPC noted that growth in deposits remained robust, while loans continued to grow albeit at a moderate pace. Local currency deposits grew by 11.4 per cent at April 2024, a deceleration relative to growth of 13.2 per cent at April 2023, consistent with the deceleration in nominal GDP growth. The flow of new loans to the private sector increased in real terms by 0.6 per cent in April 2024.

- The domestic banking system remains sound, with adequate capital and liquidity.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near term.

- The MPC noted that future monetary policy decisions will continue to depend on incoming data, which, if they indicate a sustained anchoring of inflation within the target range, could lead to further easing of monetary policy.

_______________________

Chairman of the MPC

28 June 2024