Summary of

Monetary Policy Discussion and Decisions

December 2023

At its meetings on 18 and 19 December 2023, the Monetary Policy Committee (MPC) noted the following:

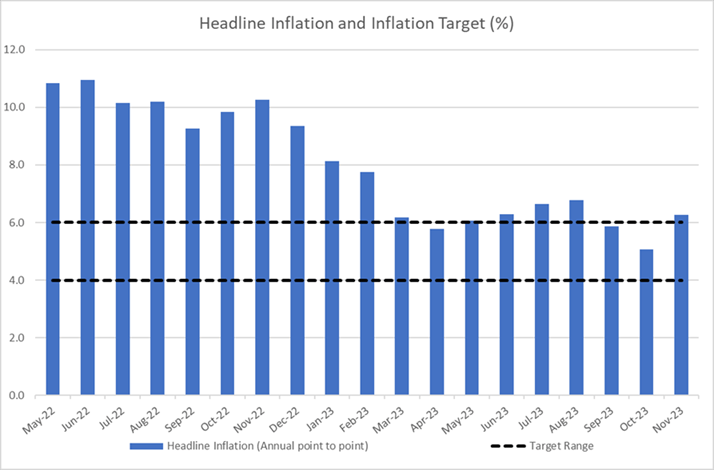

- Jamaica’s annual headline inflation rate at November 2023 of 6.3 per cent, which was outside the Bank’s target range of 4.0 to 6.0 per cent, was above the 5.1 per cent recorded at October 2023 but was much lower than the peak rate of 11.8 per cent recorded at April 2022. Core inflation (which excludes food and fuel prices from the Consumer Price Index (CPI)) was 5.6 per cent at November 2023, generally in line with the average for the past three months and lower than the 8.4 per cent recorded at April 2022. This trend suggests that core inflation is being contained, which bodes well for the longer-term inflation outlook.

- The key drivers of headline inflation, such as international commodity prices and shipping costs, continued to decline, and the exchange rate has remained generally stable, given the monetary policy actions as well as strong tourism and remittance inflows. Consistent with these trends, deposit dollarisation, which reflects the proportion of United States (US) dollar deposits to total deposits, continued to trend downward to its lowest level since December 2011. With regard to commodity prices, international oil prices have trended below the Bank’s forecast, mainly due to the weaker-than-forecasted impact of production cuts by major oil producers. Average grains prices were also well below the Bank’s forecast and are expected to remain below projections over the near term. Inflation in the economies of Jamaica’s main trading partners has also continued to decline.

- As anticipated by the Bank, the uptick in headline inflation in November 2023 was primarily driven by the impact of an increase in public passenger vehicle (PPV) fares announced by the Government. This is in addition to high domestic agricultural price inflation due to continued adverse weather conditions. The increase in inflation in November, consequent on these factors, marks the onset of temporary fluctuations in inflation outside the target band.

- Inflation is projected to continue to rise above the Bank’s target range for much of the period between the December 2023 and March 2025 quarters, primarily due to the continued impact of the increases in selected PPV fares. Without the effects of the PPV fare increase, it is estimated that annual headline inflation would have averaged 5.9 per cent during this period.

- The risks that inflation could be higher than forecasted are elevated. These risks include second-round effects from the PPV fare increases, sharper-than-anticipated increases in domestic agricultural price inflation over the near term, and higher-than-projected future wage adjustments in the context of the tight domestic labour market. A deterioration in supply chain conditions could also influence higher inflation. The main downside risks, which could lead to lower inflation, include the possibility that oil and grains prices could trend well below the forecast. Other downside risks also include weaker-than-expected global growth, which could have a stronger-than-projected downward pull on domestic demand and imported inflation, resulting in lower levels of price changes.

- Against the background of these developments, the MPC unanimously agreed to maintain: (i) the policy interest rate at 7.0 per cent, (ii) tight Jamaican dollar liquidity conditions, and (iii) relative stability in the foreign exchange market.

The following considerations also informed the MPC’s decisions:

- The Jamaican economy continues to expand, which supports increases in aggregate demand for goods and services. Despite the impact of drought conditions on the agriculture sector, gross domestic product (GDP) for the September 2023 quarter is estimated to have grown within the range of 1.0 to 3.0 per cent, and there are signs that the economy continued to expand in the December 2023 quarter. The notable decline in the unemployment rate as at July 2023 to 4.5 per cent, supported by anecdotal information about wage adjustments in selected private sector industries, indicates that the domestic labour market remains very tight.

- The risks to the domestic GDP forecast are skewed to the downside, which means that actual GDP growth could be lower than the forecast. Growth in tourist arrivals and related activities could be adversely affected by headwinds to global growth. There is also a risk that domestic consumer spending could be negatively affected by the larger-than-forecasted impact of domestic inflation.

- US GDP growth for 2023 is now projected to be higher than previous projections, but is still projected to slow in 2024. This prediction is generally consistent with consensus forecast. This outlook reflects the impact of high, albeit decelerating, inflation on consumption, tight monetary conditions and reduced fiscal support. Inflation in the US was 3.1 per cent at November 2023, a decline relative to the September 2023 outturn of 3.2 per cent. US inflation is projected to continue its general fall as the economy slows but remain above the US Federal Reserve’s (Fed) target of 2.0 per cent for the remainder of 2023 and 2024.

- As anticipated, the Fed continued to maintain its monetary policy target for interest rates at 5.25 to 5.50 per cent in December 2023, following its last increase in July 2023. The Fed also suggested that future monetary policy decisions will continue to be data-dependent. Consensus forecast is for the Fed to begin cutting rates by April 2024.

- The outturns for selected external indicators have been below the Bank’s projections, for the most part. The average of daily West Texas Intermediate (WTI) crude oil prices for October and November 2023 declined by an average of 6.9 per cent, lower than the Bank’s forecast for an increase, while there was an increase in Liquified Natural Gas (LNG) prices for the same period of 6.7 per cent, which was higher than the Bank’s forecast. The decline in average WTI prices occurred in the context of an increase in US inventories and the lower-than-anticipated impact of the conflict in the Middle East. International fertiliser prices declined by an average monthly rate of 2.7 per cent for October and November 2023. Similarly, the decline in average grains prices (wheat, corn, and soybean) was larger than projected for the period.

- The risks to the outlook for the US economy are balanced. Lower growth could emanate from escalating geopolitical tensions, increased supply shortages, a stronger-than-projected impact of contractionary monetary policy, and the tightening of credit conditions on economic growth. However, higher-than-projected increases in consumption spending could support higher GDP growth.

- The MPC continues to see a relatively strong, lagged pass-through of its policy rate to interest rates in the domestic money and capital markets and the term rates offered on deposits by deposit-taking institutions (DTIs). The upward adjustment in market rates and time deposits has slowed, consistent with the MPC’s pause in interest rate increases. The DTI sector also continued to make small changes to rates on saving deposits and new mortgage loans. However, the weighted average loan rate declined marginally in October 2023. The flow of new loans to the private sector increased in real terms by 12.6 per cent over the year to October 2023, notwithstanding a tightening in credit terms, as indicated by DTIs in Bank of Jamaica’s Quarterly Credit Conditions Survey. Local currency deposits grew by 15.4 per cent at October 2023, an acceleration relative to 13.2 per cent in April 2023 at the start of the fiscal year, and was above the estimated growth in nominal GDP for the December 2023 quarter. Some of this growth is consistent with a fall in foreign currency deposits, given the stability in the exchange rate associated with the recent current account surplus of the balance of payments and the Bank’s policy actions. Consequently, deposit dollarisation continued to trend downward, showing an increasing preference to hold Jamaican dollars.

- The domestic banking system remains sound, with adequate capital and liquidity.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near term.

- The MPC noted that future monetary policy decisions will, therefore, critically depend on incoming data related to the strength of the potential risks to inflation noted above. The Committee decided to maintain heightened surveillance of these risks and core inflation. The MPC is prepared to take the necessary actions, including further tightening of monetary policy, if the emerging upside risks to inflation highlighted above materialise.

_____________________

Chairman of the MPC

20 December 2023